As the new FRS102 changes have started to be implemented, it is important to be aware of several important Company Law updates. A summary of some of the key changes are set out below:

Small and micro companies exemption not to file their profit and loss account

Previously, the government had set up plans to mandate from April 2027 the filing of the profit and loss account for micro companies, and the directors’ report, auditor’s report and profit and loss accounts for small companies (in other words, the full accounts for those size companies).

However, this has now been put on hold. The government has indicated that the proposal is still under consideration and, they will provide companies at least 21 months’ notice of any changes. Therefore as it stands, this will not likely come in until at least 2028, if it goes ahead at all.

Changes to company/LLP size thresholds for periods commencing on or after 6 April 2025

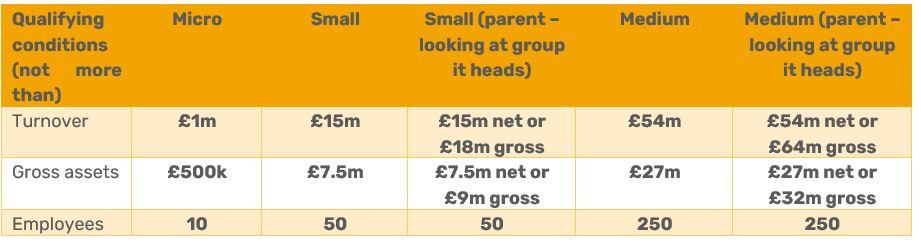

With it being almost a year since these changes came into effect, they will soon start applying to most upcoming accounting periods. A reminder of the new thresholds:

When the new thresholds start to apply, the entity needs to look at their size afresh as if the thresholds had always applied and therefore when considering the two out of three thresholds for two consecutive periods rule, it should be based solely on the new thresholds irrespective of the size they were previously based on the old thresholds.

As with previously, the parent thresholds above look at the figures of group/sub-group the parent entity heads irrespective of whether consolidated accounts are prepared at level. “Net” refers to after intercompany eliminations and “Gross” is before intercompany eliminations and it’s a choice of which to use.

Note that the recognition of right of use assets upon the implementation of the new FRS102 may have a further impact on entities’ size classification.

Removal of some directors’ report disclosures for periods commencing on or after 6 April 2025

Many of the disclosures in directors’ reports which will no longer be required from the same time as the new size thresholds took effect. This is due to many of these being duplicated either in strategic report requirements or in the accounts themselves. The disclosures being removed are as follows:

However, the Streamline Energy and Carbon Report (SECR) requirements, which previously only applied to large companies based on the large thresholds, has not had its thresholds change and therefore will apply to some medium companies under the new thresholds (i.e. those who would have been large under the old thresholds).

Guiding you through the changes

At HW Fisher, our FRS 102 experts can help guide your business through the changes. Contact us for support.

We’d love to hear from you. To book an appointment or to find out more about our services: